Introduction

Across corporate real estate and facilities management, artificial intelligence has rapidly shifted from an abstract concept to an operational reality. In just a few years, AI has moved beyond experiments and pilots to become a functional layer embedded in portfolio optimization, occupancy analytics, performance management, operations, and even sales. Today, the question for corporate real estate leaders is no longer if AI will play a role, but about understanding what AI solutions are right for their organization, how effectively they are being applied, how deeply they are integrated, and how they are reshaping clients and occupier expectations.

AI is now influencing decisions across the entire real estate value chain. Adoption is accelerating, yet executional maturity varies widely. Some organizations are achieving measurable operational gains, while others remain stalled by fragmented systems, legacy workflows, and unclear data strategies.

As the industry enters a new phase of digital transformation. An emerging “AI baseline” is defining the minimum digital capabilities and intelligence required to remain competitive, efficient, and aligned with enterprise goals. Understanding what now constitutes table stakes, and where early adopters are already moving ahead, is essential for any CRE or facilities organization seeking to modernize its operations.

This three-part series explores that evolution. Part 1 examines current AI trends and adoption patterns, highlighting what’s driving momentum and where organizations are struggling. Part 2 outlines practical strategies to close the AI readiness gap and align technology investments with business goals. Part 3 looks ahead to the next frontier - how leading organizations can move beyond the AI baseline toward a more intelligent, connected, and adaptive future of real estate.

The New AI Baseline - Trends Defining CRE

AI is undeniably here to stay. Yet amid its rapid evolution, the corporate real estate industry is showing early signs of imbalance between hype and practical adoption. The development of AI tools and solutions is accelerating faster than meaningful client demand and, in many cases, faster than the organizational readiness required to apply them effectively.

Many organizations understand AI’s high-level potential for automation, analytics, and efficiency, but many struggle to translate that awareness into actionable implementation. Moving from conceptual understanding to piloting, resourcing, and scaling AI solutions remains a significant challenge. As a result, many organizations find themselves in an environment where opportunity and constraint coexist: the tools are available, but their impact is limited by fragmented systems, unclear data strategies, legacy workflows, and constrained budgets.

Recent surveys reinforce this reality. While nearly all firms report having adopted or planning to adopt AI, more than 90% cite barriers to tangible execution (McKinsey, 2025), including limited internal expertise, budget constraints, bespoke data quality, and inadequate integration across platforms. Many of these challenges stem from years of under investment in foundational building systems and application infrastructure, leaving organizations unprepared for the data-driven discipline that effective AI deployment requires.

In November 2025, McKinsey published a global survey offering a clearer view of the current AI landscape, adoption challenges, and maturity levels across industries. The survey includes 1,993 respondents spanning Technology, Media and Telecom, Healthcare, Energy and Materials, Manufacturing, Professional Services, Travel and Logistics, Pharmaceutical, Engineering and Construction, Financial Institutions, and Retail.

In the next section, we translate several of the survey's findings into practical insights. We explore what’s really taking shape with AI adoption across the industry, how organizational size, and functional vs. Enterprise-level deployment influences readiness, and how maturity along the adoption life-cycle is driving different outcomes.

Source: McKinsey Global Surveys on the state of AI, 2017–2025

Source: The state of AI in 2025 – Agents, innovation, and transformation, QuantumBlack AI by McKinsey, November 2025

Summary of Key Takeaways

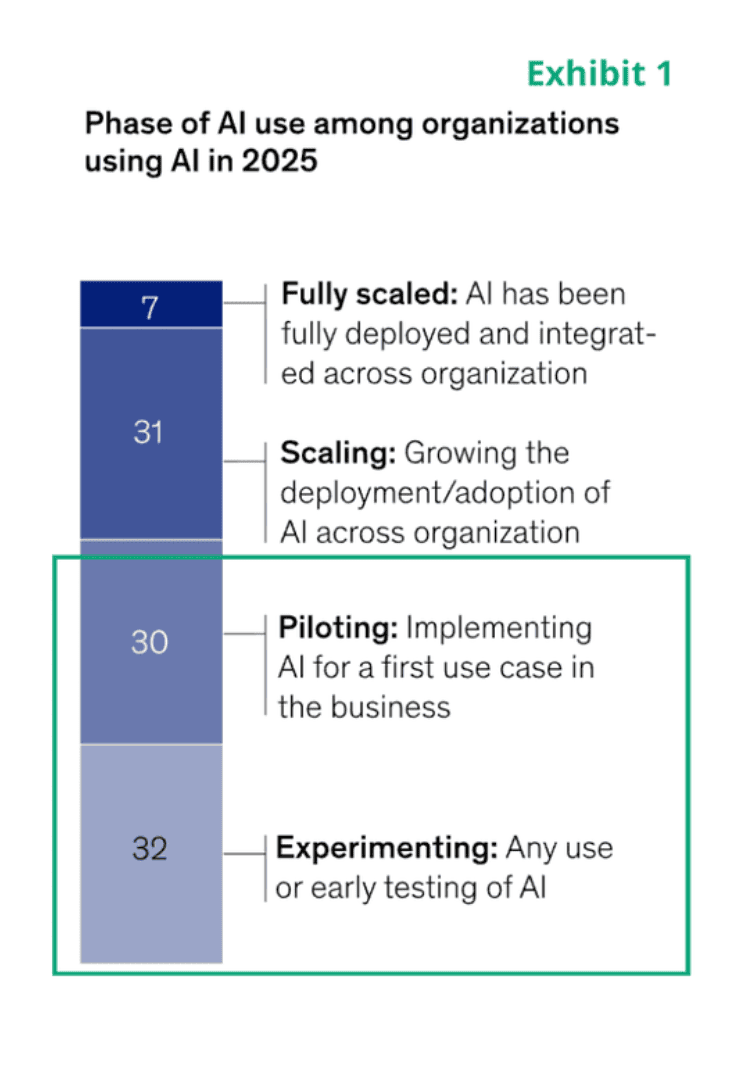

- While all surveyed respondents report their organization are using AI, and many have begun to explore AI agents, the headline overstates the true level of adoption. This apparent ubiquity is misleading as nearly two-thirds say their organizations remain stuck in the experiment and pilot phase (Exhibit 1 – Overall Percentage of Organizations Adopting and Maturing AI by Life-Cycle Phase). And fewer than 10% report scaling AI within any individual business function (Exhibit 2 – Percentage of Respondents Scaling AI by Company Revenue).

- Organization size plays a decisive role in determining AI maturity (Exhibit 3 – Phase of Organization’s Use of AI by Company Revenues). Large enterprises, particularly those with revenue above $1B, are far more likely to possess the structural maturity, data readiness, and transformation resources required to deploy AI at scale and realize meaningful returns. By contrast, mid-market and smaller firms often adopt AI "in principle" but struggle to move past pilot paralysis due to familiar barriers - limited standards and data governance, fragmented or insufficient data types, inconsistent operating models, narrow or unaligned use cases, and underdeveloped enterprise strategies.

- Across respondents, more than two-thirds indicate that efficiency (reducing costs) was the main AI enterprise objective. Growth and Innovation and Business Model Transformation remain secondary or tertiary priorities. (McKinsey, 2025) With use cases on efficiency rather than transformation, the workforce impact does not appear to be a straightforward automation story. Instead, expectations point to a gradual transition, and this includes changes to the workforce. Organizations foresee a shift in the mix of job types, with fewer task-based roles and continuing to favor more skilled and supervisory positions vs a large job displacement. Looking forward into 2026, respondents shared their outlook on workforce changes: 32% anticipate a decrease in workforce size; 43% expect no change; and 13% expect an increase. (McKinsey, 2025)

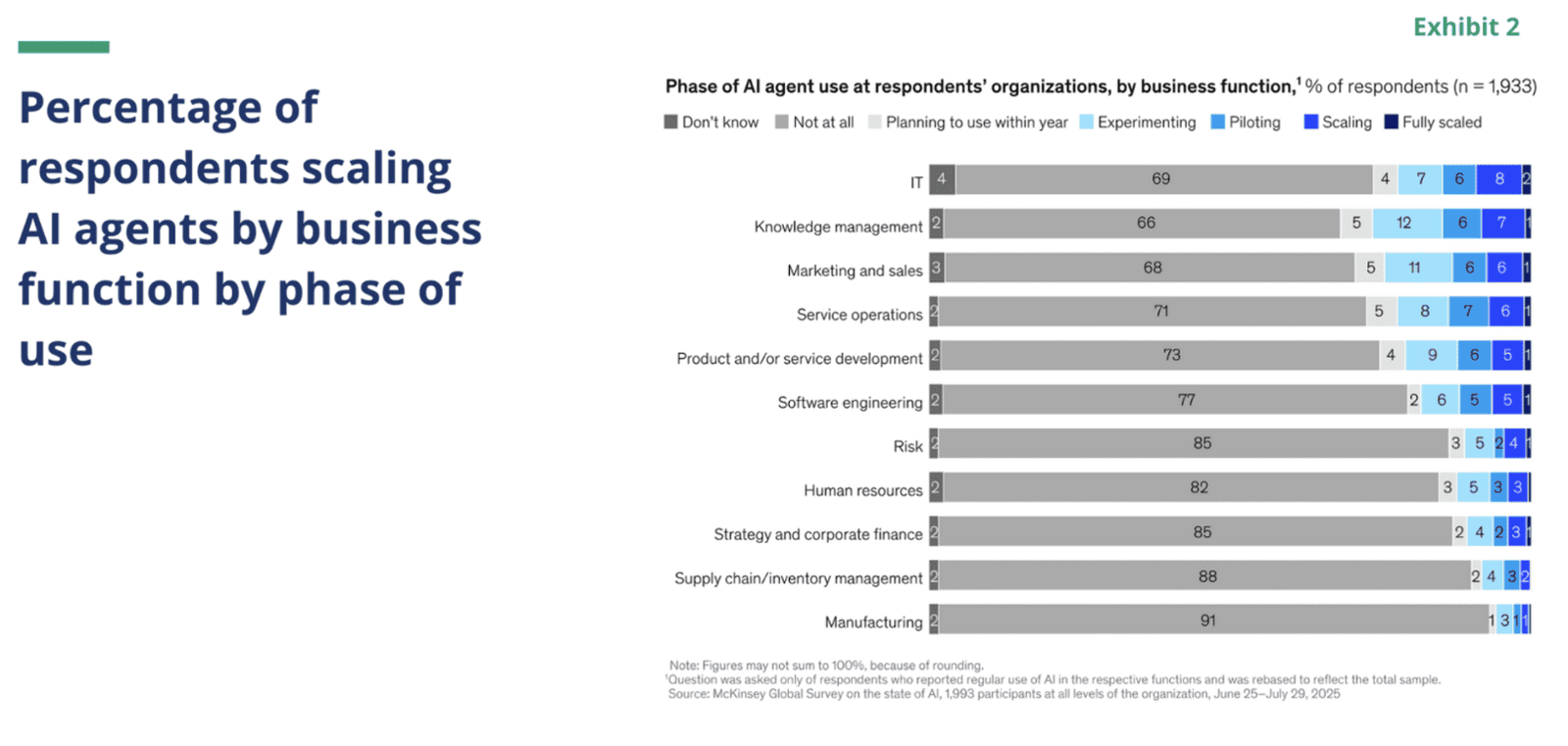

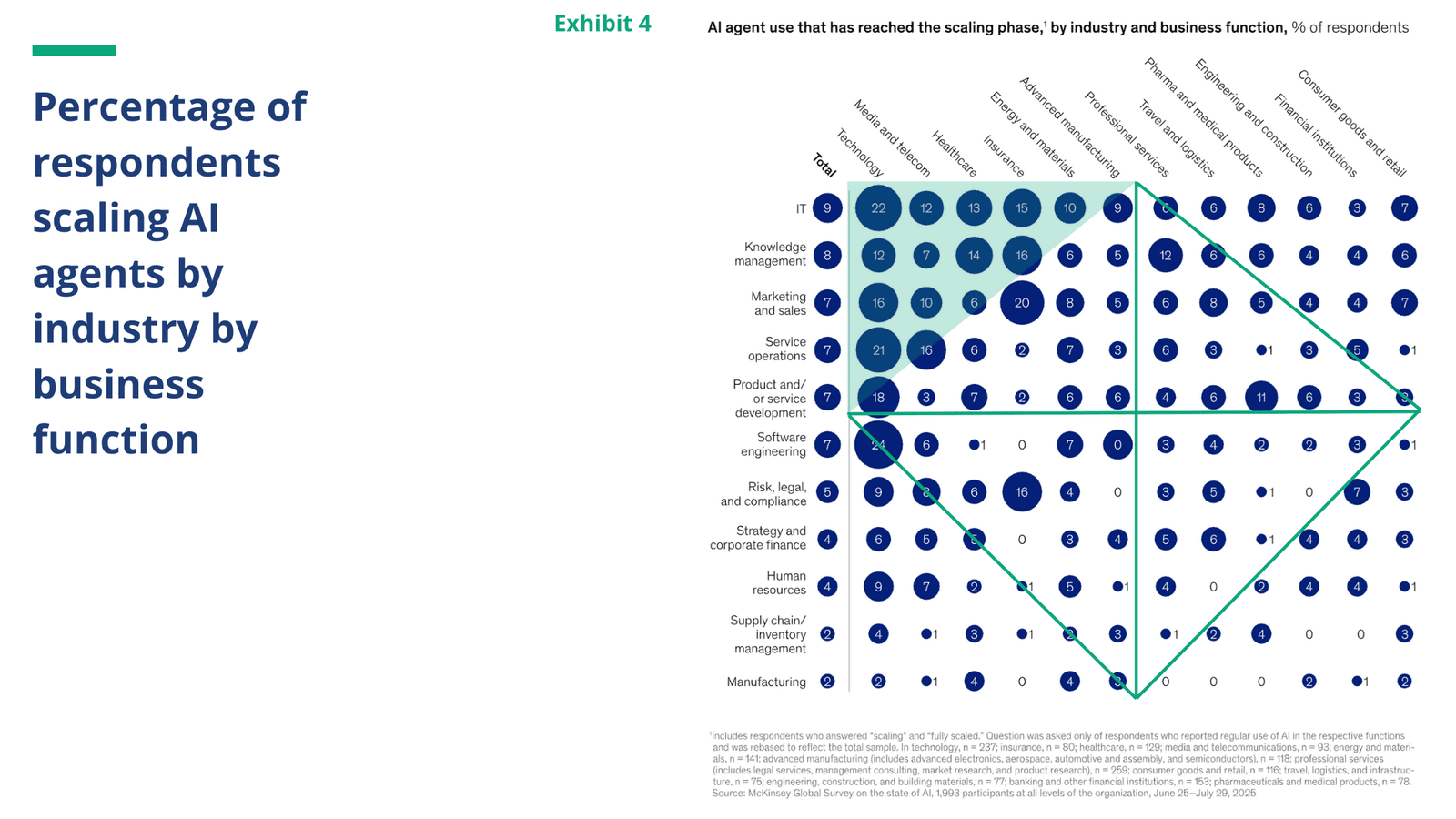

4. In examining AI demographics, current state utility across industries, and adoption by business function, (Exhibit 4 – Percentage of Respondents Scaling AI by Industry by Business Function) presents a heat map illustrating which industry segments and functions are progressing toward the scaling phase. A key insight emerged from the analysis is the presence of three distinct clusters of adoption and correlation, each accelerating along a different path shaped by data maturity, regulatory context, and operational complexity

Three industry groups evolving AI from incremental adoption to transformative revolution

Group 1 - Technology, Media, and Telecom (Digital Industry Vertical)

Group 2 - Healthcare and Insurance (Regulated and Risk Industry Vertical)

Group 3 - Industrial and Resources (Operational Industry Vertical)

Technology, Media, and Telecom operate as inherently data-driven industries and consistently demonstrate higher AI value. Their early adoption patterns, strong use-case profiles, and mature data ecosystems position them as data-rich verticals. Their AI maturity is elevated by their digital-first business models, emphasis on customer engagement, and use cases that naturally align with automation analytics and enhanced human experience.

Healthcare and Insurance follow risk-driven models, resulting in slower but steady AI adoption. These sectors have strong potential in areas such as underwriting, fraud detection, diagnostics, and care optimization. However, Healthcare adoption in particular is constrained by regulatory complexity, privacy requirements, and stringent governance frameworks.

Industrials and Resources is a group that spans advanced manufacturing, energy, and materials – all asset intensive sectors. Their AI maturity is comparatively lower with use-cases centered on physical systems and data from building and equipment maintenance. Adoption is likely constrained by regulatory obligations, data variability, operational complexity, and the influence of long capital investment cycles.

In 2025, nearly 90% of respondents report using AI in at least one business function. However, as shown in (Exhibit 5 - Percentage of Respondents Deploying AI Across Business Functions), adoption drops sharply as organizations attempt to scale. While 51% deploy AI across three or more functions (a 73% decline from single-function adoption), only 20% report deployment across five or more functions, reflecting a dramatic 340% decline.

In short, AI adoption is broad, but depth and scale remain limited, underscoring the operational and organizational challenges companies face. Key implications include:

Process mapping – before automating workflows or designing processes, organizations must understand – and often redesign - their business processes. Clear mapping of how processes interconnect and should interconnect is essential to create a target operating model that leverages automation, structured data, and AI. A new "blueprint for change" is required to unlock the full impact of workflow automation and data-enable decision-making. Deployment complexity – scaling AI beyond a single function introduces integration challenges across processes, systems, and teams. This creates friction, increases change management demands, and heightens the risk of fragmentation. Organizational readiness – few organizations have the expertise, governance structure, or data foundation required to support multi-function AI deployment. Limited internal skills, unclear ownership, and gaps in data infrastructure continue to constrain maturity. Value realization – enterprise-level value differs from functional value. The steep drop-off shown in Exhibit 5 highlights that many organizations struggle to achieve cross-functional or enterprise-wide impact. AI investments are often isolated within individual functions, preventing organizations from realizing broader operational or strategic benefits.

Source: McKinsey Global Surveys on the state of AI, 2017–2025

Source: The state of AI in 2025 - Agents, innovation, and transformation, QuantumBlack AI by McKinsey, November 2025